Latest World Air Transport Statistics highlights robust passenger demand, expanding premium travel, stronger fleet utilisation and continued recovery across global aviation

The International Air Transport Association (IATA) has released its 2025 World Air Transport Statistics (WATS), revealing another year of sustained growth for the global aviation industry. The latest report highlights rising passenger demand, continued expansion in premium-class travel, evolving aircraft utilisation and the dominance of Asia-Pacific in the world’s busiest air travel corridors. The findings are based on operational and financial data collected from 1,315 airlines, including more than 250 international carriers, making WATS one of the aviation industry’s most comprehensive statistical references. The data has been verified through IATA’s official publication.

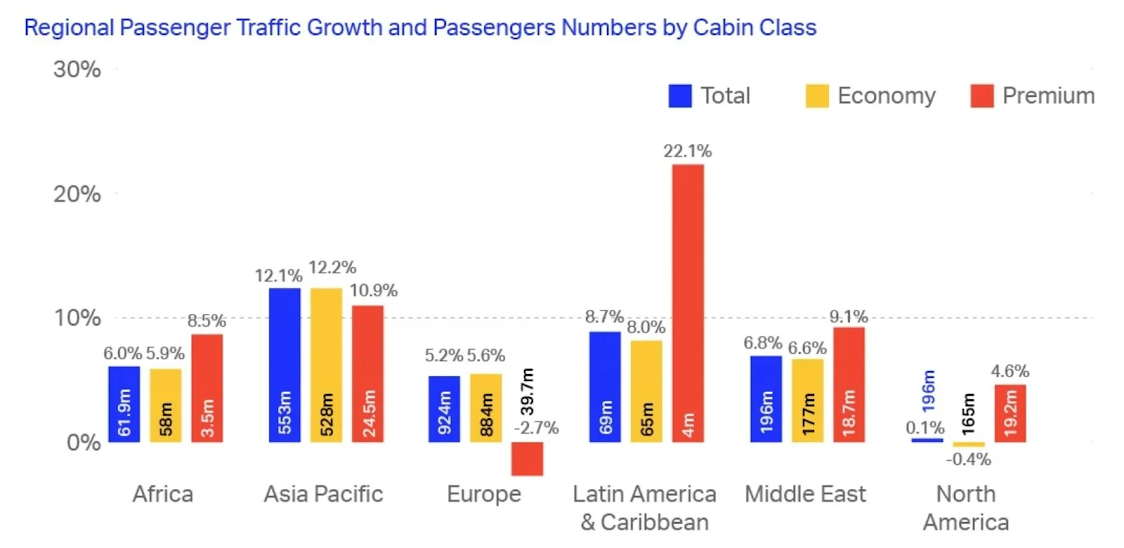

Premium travel continues to outperform

International premium-class travel maintained its upward trajectory in 2025, reflecting sustained demand from both business and high-value leisure travellers.

According to the report, 109.7 million passengers travelled in business or first class on international services during the year, representing a 4.5% increase compared with 2024. Premium travellers accounted for 5.5% of all international passengers, underlining the resilience of the premium travel segment despite ongoing economic uncertainty.

Latin America recorded the strongest year-on-year growth in premium travel, with passenger numbers increasing 22.1% to reach 4 million travellers.

Europe remained the world’s largest premium-class market, serving 39.7 million premium passengers, while North America recorded the highest proportion of premium travellers relative to total international traffic at 10.4%, followed closely by the Middle East at 9.5%.

Asia-Pacific dominates the world’s busiest air corridors

The report confirms that domestic aviation continues to drive global passenger volumes, particularly across Asia-Pacific.

The Jeju–Seoul Gimpo route in South Korea retained its position as the world’s busiest airport pair in 2025, carrying 13.3 million passengers during the year.

Remarkably, nine of the world’s ten busiest airport pairs were located within the Asia-Pacific region, with Jeddah–Riyadh in Saudi Arabia standing as the only non-Asia-Pacific route to feature in the global top ten. All of the busiest airport pairs were domestic services, highlighting the continued strength of large domestic aviation markets.

Biggest Passenger Markets by Country in 2025

| Country | Passenger Numbers | Change % YoY |

|---|---|---|

| United States | 890.1m | +1.6% |

| China (People’s Republic of) | 776.1m | +4.8% |

| United Kingdom | 269.7m | +3.4% |

| Spain | 252.7m | +5.0% |

| Japan | 223.5m | +9.2% |

| India | 218.2m | +3.3% |

| Italy | 187.3m | +5.8% |

| Germany | 163.8m | +3.4% |

| France | 152.6m | +2.2% |

| Türkiye | 129.3m | +2.9% |

*Figures include scheduled passengers originating or terminating in each country. Domestic journeys are counted once; international journeys are counted in both the origin and destination countries.

Regional leaders also reflected strong domestic demand worldwide:

- Africa: Cape Town – Johannesburg carried 3.4 million passengers.

- Latin America: Bogotá – Medellín handled 3.5 million passengers.

- Europe: Barcelona – Palma de Mallorca remained the continent’s busiest route with 2.1 million passengers, while Stockholm–Malmö recorded Europe’s fastest growth, with traffic surging 85%.

- North America: New York JFK – Los Angeles remained the busiest domestic route with 2.2 million passengers, while JFK–London Heathrow was the region’s leading international connection with 2.1 million travellers.

United States retains largest passenger market

The United States remained the world’s largest aviation market in 2025, recording 890.1 million originating and terminating passengers, although growth slowed to 1.6%, the weakest among the world’s ten largest aviation markets.

China retained second place with 776.1 million passengers, representing annual growth of 4.8%.

Other major passenger markets included:

- United Kingdom – 269.7 million

- Spain – 252.7 million

- Japan – 223.5 million

- India – 218.2 million

- Italy – 187.3 million

- Germany – 163.8 million

- France – 152.6 million

- Türkiye – 129.3 million

Among emerging markets, Kazakhstan posted one of the strongest growth rates globally, with passenger traffic increasing 40% to 18.1 million, while Uzbekistan expanded 16.9% to 12.5 million passengers.

Vietnam also continued its rapid aviation expansion, handling 80.9 million passengers, an increase of 14.8% over the previous year.

Modern aircraft continue reshaping airline fleets

The WATS report also highlights the ongoing transition towards newer, more fuel-efficient aircraft.

Among widebody fleets, the Airbus A350 recorded the strongest long-term growth, with flights increasing 117.4%between 2019 and 2025, while operations by the Boeing 787 Dreamliner rose 40.8% over the same period.

The Airbus A220 experienced the fastest expansion of any aircraft family, with flight activity increasing more than 770%, reflecting its growing adoption by airlines on regional and medium-haul routes.

Conversely, operations involving the Airbus A380 continued to decline, with flights down 24.4% compared with pre-pandemic 2019 levels, illustrating the industry’s gradual shift towards smaller, more efficient aircraft.

Narrowbody aircraft remained the backbone of global aviation. The Boeing 737 family operated 10.8 million flightsduring 2025, maintaining its position as the world’s most utilised aircraft type, followed by the Airbus A320 with 8.7 million flights and the Airbus A321, whose operations increased 61.6% since 2019 to reach 4.2 million flights.

Most Used Aircraft Types

The Changing Face of the Global Fleet

| Aircraft type / Model | Number of Flights 2025 | Number of Flights 2019 | Change 2019-2025 |

|---|---|---|---|

| Narrow Body / Boeing 737 | 10.8m | 10.5m | +3.1% |

| Narrow Body / Airbus A320 | 8.7m | 8.1m | +7.6% |

| Narrow Body / Airbus A321 | 4.2m | 2.6m | +61.6% |

| Narrow Body / Embraer ERJ170/190 | 2.7m | 2.6m | +2.8% |

| Narrow Body / Airbus A319 | 1.4m | 2.1m | -34.3% |

| Wide Body / Boeing 787 | 795k | 564k | +40.8% |

| Narrow Body / Airbus A220 | 530k | 61k | +770.4% |

| Wide Body / Airbus A350 | 434k | 200k | +117.4% |

| Wide Body / Airbus A380 | 90k | 119k | -24.4% |

Industry recovery gathers pace

The latest statistics underline aviation’s continued recovery and long-term growth trajectory. Strong premium travel demand, expanding domestic markets, increasing adoption of next-generation aircraft and sustained passenger growth across both mature and emerging markets demonstrate the industry’s resilience despite ongoing geopolitical and economic challenges.

As airlines continue investing in fleet modernisation, network expansion and operational efficiency, IATA’s latest data suggests global aviation is entering a new phase of sustainable growth, supported by rising international connectivity and renewed consumer confidence in air travel.

{kind=link}